|

|

|

Issue No. 006 | Friday, June 5, 2026

|

|

|

Was this forwarded to you?

Subscribe free at manufacturingmonitor.com

|

|

Today's Clock-In

Two June 1 events told the same reshoring story from different angles.

The White House adjusted Section 232 tariffs in a way that favors US-located manufacturing in HVAC, agricultural equipment, industrial machinery, and grid equipment. That same morning, the ISM Manufacturing PMI printed 54% for May, its highest reading since May 2022 and its fifth consecutive month of expansion.

The policy signal and the factory signal are starting to line up.

Also this week: Ford Energy landed its first stationary-storage customer, Tesla has deployed more than 1,000 Optimus humanoid robots across its manufacturing footprint, GE Aerospace plans another 5,000 US hires, and Boeing received clearance to raise 737 MAX output to 47 aircraft per month.

In this issue, we'll get into

- How Section 232 became more targeted

- Why Ford's EV battery capacity is turning into a data-center storage play

- How battery energy storage cells actually get made

- Why Odd Lots is one of the best manufacturing podcasts hiding in plain sight

|

|

Quick Hits

Ford Energy landed its first stationary-storage customer.

EDF Power Solutions North America will procure up to 4 GWh per year from Ford's Glendale, Kentucky plant beginning in 2028. Ford Energy is now targeting 20 GWh per year of battery storage capacity, and Ford stock hit a three-year high on a reported $10B valuation for the unit.

The important part is not just that Ford found a customer. It is that Ford appears to be converting EV battery capacity into grid and data-center storage capacity. That is a cleaner growth story than waiting for EV demand to absorb everything.

Tesla has deployed more than 1,000 Optimus robots across its manufacturing footprint.

The highest concentration is reportedly at Giga Texas. Fremont is being converted into a first-generation Optimus production line targeting 1M units per year by the end of 2026, while a second-generation Giga Texas facility is targeting 10M units per year by 2027.

Whether those production targets prove realistic is a separate question. The bigger point is that Tesla is turning its own factories into the test environment for humanoid automation. That may matter more than the early unit economics.

GE Aerospace plans another major hiring wave.

GE Aerospace plans to hire 5,000 US workers in 2026, on top of the 5,000 it hired in 2025. The company is also making a €110M investment across European manufacturing and adding more than 1,000 European workers this year.

Aircraft demand is still running well ahead of supply. With Boeing and Airbus backlog now sitting around twelve years, GE's hiring plan is not a cyclical footnote. It is another signal that aerospace capacity is being rebuilt one shift, one supplier, and one facility at a time.

Boeing has been cleared to raise 737 MAX production.

Boeing can raise 737 MAX output from 42 to 47 aircraft per month, while the MAX 7 and MAX 10 continue through final certification. Boeing delivered 143 aircraft in Q1 2026, its strongest quarter in years. Airbus delivered 114, down 16% year over year, partly due to Pratt & Whitney engine shortages.

The aircraft market is still not normal. Demand is there. Backlog is there. The constraint is the production system.

|

|

Lead Story

PMI 54, and Section 232 Just Learned How to Aim

Two of this week's most important manufacturing data points share a date.

On June 1, the White House signed a new Section 232 proclamation that changed how tariffs apply to steel, aluminum, and copper-intensive products. The same morning, the ISM Manufacturing PMI printed 54% for May, its highest reading since May 2022 and its fifth consecutive month of expansion.

Most coverage treated those as separate stories.

They are not.

|

What's Section 232?

Section 232 of the Trade Expansion Act of 1962 authorizes the President to impose tariffs or quotas on imports that the Department of Commerce determines threaten national security. It is the legal basis for the steel and aluminum tariffs first imposed in 2018, was expanded to copper earlier this year, and gets periodically revised by proclamation. June 1 is the most recent revision.

|

The Section 232 update keeps the headline 50% rate for products substantially made of steel, aluminum, or copper. But the new structure is more targeted than a simple across-the-board tariff. A reduced 15% transitional rate applies to selected categories, including metal-intensive industrial machinery, agricultural equipment, residential HVAC systems, and electrical grid equipment.

A 10% rate applies to products made abroad with American metals. The qualifying threshold for products made entirely from US metal drops from 95% to 85%. Products with less than 15% steel, aluminum, or copper content fall out of Section 232 entirely.

That is not just tariff policy. It is industrial policy.

The new structure does three things at once. It punishes finished-metal imports. It gives selected categories a more favorable rate when the administration wants domestic capacity. And it reduces friction for companies using American metals in multi-country supply chains.

That last point matters. A lot of manufacturers do not operate in a clean domestic-or-imported world. They source, fabricate, finish, and assemble across borders. The 85% threshold is still difficult, but it is more realistic than 95%.

PMI 54 is the receipt.

New orders, production, and employment all moved in the same direction. Kearney now puts cumulative US onshoring investment at roughly $3T. That figure is messy because it includes a mix of announced projects, projects under construction, and completed capacity. But the direction is no longer easy to dismiss.

For several years, reshoring could be treated as press-release theater.

That argument is getting harder to make.

The cleanest read is that policy is starting to move in lockstep with capex. HVAC is the easiest example. Last week, we wrote about thermal management becoming a front-line manufacturing category for the AI buildout. This week, the Section 232 update explicitly reduces tariff pressure on residential HVAC systems and components, electrical grid equipment, and certain industrial machinery.

Those are not random categories.

They are the physical bottlenecks the AI infrastructure cycle keeps revealing: cooling, power, metals, equipment, and factory throughput.

That does not mean the policy is automatically good.

A 50% tariff is still a 50% tariff. Manufacturers that specify steel coil, aluminum sheet, copper articles, or finished metal components will still absorb cost or push it through the chain. The 85% US-content threshold is easier than 95%, but still excludes many real-world sourcing situations. And every category-specific rate eventually creates classification disputes that must be argued in front of Customs.

The policy is more targeted.

It is not simpler.

The corporate stories this week reinforce the same point from the operating side. Ford is converting battery capacity toward stationary storage. Tesla is pushing humanoid robots into its own factories. GE Aerospace is hiring thousands to support a decade-plus aircraft backlog. Boeing is increasing MAX production.

These are not all policy stories.

They are capacity stories.

That is the thread running through the week. Washington is trying to steer capacity. Manufacturers are trying to secure capacity. Customers are trying to buy capacity before someone else does.

The hard part is what comes next.

The 15% transitional rate sunsets at the end of 2027. CHIPS-era subsidies were tied to schedules. Section 232 carve-outs are tied to political will. Any manufacturer building US capacity right now is making a bet on demand, cost, labor, supply chain resilience, and policy persistence at the same time.

That is uncomfortable.

But it is now legible.

Industrial strategy is becoming part of the engineering spec.

Key Numbers

|

ISM Manufacturing PMI, May

54%

highest reading since May 2022

|

|

Section 232 transitional rate

15%

HVAC, ag, industrial, grid equipment, through 2027

|

|

Cumulative US onshoring

~$3T

Kearney estimate of factory investment to date

|

Sources:

White House Section 232 proclamation,

ISM May 2026 Manufacturing PMI,

C.H. Robinson advisory,

HVAC/ag/industrial carve-out detail.

|

|

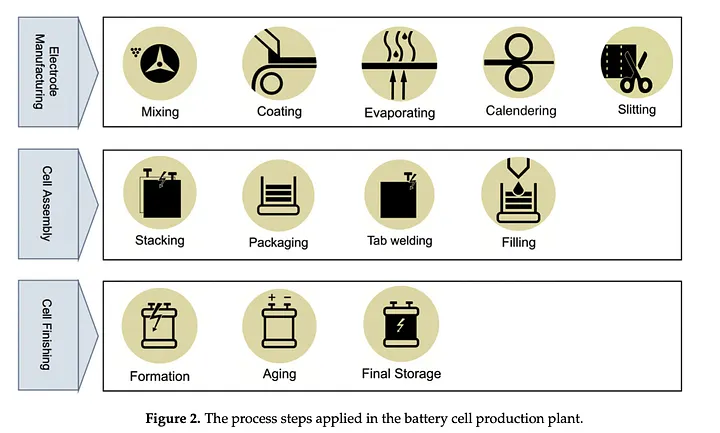

How It Works

How a Battery Energy Storage Cell Gets Made

Stationary-storage batteries use the same basic lithium-ion manufacturing process as EV batteries. The difference is the optimization target.

EV cells are engineered around energy density, weight, range, and fast charging.

Stationary-storage cells are engineered around cycle life, cost per kWh, safety, manufacturability, and long-duration performance.

The process is still brutally precise.

1. Mix the slurry.

The process starts with electrode slurry. Cathode materials such as NMC or LFP are mixed with conductive additives, binder, and solvent. Anode materials, usually graphite-based, are mixed separately. Particle distribution and viscosity matter because every downstream step depends on a consistent slurry.

If the mix is wrong, the defect is already inside the cell before the cell exists.

2. Coat the foil.

Cathode slurry is coated onto aluminum foil. Anode slurry is coated onto copper foil. This is one of the first major quality-control points in the process.

Coating thickness, surface uniformity, and drying conditions all matter. Small variations can become large performance problems later.

3. Calendar to density.

The coated foils run through precision rollers that compress the electrodes to a target density. This step is called calendering.

Calendering sets porosity, adhesion, and ion transport behavior. Too much pressure can damage the electrode structure. Too little pressure can reduce energy density and consistency.

This is where mechanical precision and electrochemistry meet.

4. Slit and notch.

The coated electrode rolls are slit to the required cell width and notched to form tabs. Burrs or rough edges at this stage can create short-circuit risks later.

Battery manufacturing is full of steps that look simple until you realize the tolerances are unforgiving.

5. Assemble the cell.

The anode, separator, and cathode are stacked or wound depending on the cell format. Tabs are welded. The cell is placed into a pouch, can, or prismatic housing. The enclosure then has to be sealed.

At this point, the cell has physical form, but it is not yet a functioning battery.

6. Inject electrolyte and form the cell.

Liquid electrolyte is injected into the cell. Then the cell goes through formation cycling, which means controlled first-charge and discharge cycles.

Formation creates the solid-electrolyte interphase, or SEI layer. The SEI layer is one of the most important determinants of cycle life.

This is also one of the major bottlenecks in battery manufacturing because formation takes time and requires controlled conditions.

7. Age, test, and ship.

After formation, cells are aged under controlled temperature for days or weeks. Then they are tested for capacity, internal resistance, leakage, and self-discharge.

Cells that fail do not get cosmetically fixed.

They get recycled.

|

The manufacturing lesson

Battery cell manufacturing is chemistry, mechanical engineering, moisture control, precision coating, materials handling, and electrochemistry compressed into one production system.

The bottleneck can shift from slurry mixing to dry-room humidity, coating uniformity, calender pressure, formation throughput, or aging-rack space.

That is why Ford's Glendale pivot matters. Stationary-storage cells use the same manufacturing foundation as EV cells, but the market logic is different. If EV demand is uneven and data-center power demand is accelerating, battery capacity can be redirected toward the grid.

Same factory logic.

Different customer.

|

Sources:

Batteries Inc. process guide,

Kadant DCF on calendering.

|

|

Suggested Listening

Odd Lots, hosted by Joe Weisenthal and Tracy Alloway

Odd Lots is a Bloomberg podcast that understands something many business shows miss: the physical layer is often the real macro story.

The show has been running since 2015 and publishes three episodes per week. The format pairs financial-market analysis with guests who understand very specific parts of the real economy: traders, operators, engineers, analysts, policymakers, logistics experts, and people who spend their careers inside obscure but important corners of industry.

For Manufacturing Monitor readers, Odd Lots is useful because it often catches industrial bottlenecks before they become mainstream narratives.

Transformers. Copper. Freight. Port congestion. Semiconductor capacity. Power markets. Shipping rates. Commodity trading. Supply chain fragility.

Those topics often appear on Odd Lots before they migrate into broader business coverage.

It pairs cleanly with TBPN, last week's pick. TBPN is useful for the public-markets and venture lens on technology. Odd Lots is useful for the supply-chain, macro, and physical-economy lens behind industrial deals.

If Manufacturing Monitor is about what is happening inside factories and industrial supply chains, Odd Lots is one of the best outside sources for understanding the forces pressing on those factories from above.

Sources:

Bloomberg Odd Lots,

Apple Podcasts.

|

|

Last Pull

For most of the past decade, industrial policy and industrial reality lived in separate worlds.

One existed in Washington.

The other existed on factory floors.

This week suggests those worlds may finally be converging.

Section 232 is no longer just a tariff story. It is an attempt to steer manufacturing capacity toward specific industries. PMI suggests that capacity is expanding. Ford is repurposing battery plants. Tesla is scaling factory automation. GE Aerospace is hiring thousands. Boeing is increasing production.

The common thread is not politics.

It is capacity.

Manufacturers are no longer making decisions based only on demand forecasts, labor availability, raw material costs, and customer requirements. Increasingly, they are making decisions around policy direction as well.

Whether that lasts five years or twenty remains to be seen.

But for now, industrial strategy is becoming part of the engineering spec.

|

Reply with one line

Which category in your supply chain is being repriced by the June 1 Section 232 update, and is the new 15% transitional rate doing what the administration wants?

|

Forward this to a colleague who lives on the floor. Subscribe at manufacturingmonitor.com.

|

|