|

|

|

Issue No. 005 | Friday, May 29, 2026

|

|

|

Was this forwarded to you?

Subscribe free →

|

|

Today's Clock-In

The last two weeks were the grid and groceries. This week is the thermal layer one step closer to the rack. AI infrastructure has moved past the chip headline; the new industrial squeeze is in chillers, coolant distribution units, heat exchangers, pumps, and the water-and-power systems wrapped around them. Plus: Modine lands a $4B cooling deal, Schneider's India footprint becomes a manufacturing story, and Lockheed breaks ground on a Troy, Alabama missile plant.

|

|

Quick Hits

New week. New companies. No reruns.

- Modine disclosed a $4 billion long-term cooling agreement with an unnamed data-center operator, including a $165 million upfront payment to scale capacity; data-center sales were up 158% year over year last quarter.

- Schneider Electric expects its India data-center business to outpace the rest of its local operations over the next four to five years; data centers already make up 15% to 20% of India revenue, much of it locally manufactured.

- Lockheed Martin broke ground on an 87,000-square-foot Munitions Production Center in Troy, Alabama, supporting THAAD and Next Generation Interceptor lines as part of an $8 to $9 billion investment push through 2030.

- Airbus is warning customers of further A350 delays tied to production issues at its Kinston, North Carolina plant, the former Spirit AeroSystems site. Buying a troubled supplier asset does not instantly normalize throughput.

- U.S. energy storage hit a Q1 record of 9.7 GWh deployed, up 32% year over year per SEIA and Benchmark, with demand growth tied directly to data centers and power-price volatility.

- Stellantis is investing more than €1 billion at its Mulhouse factory to build a new generation of EVs from 2029. Europe's incumbent OEMs are still spending heavily to preserve manufacturing relevance in the next platform cycle.

|

|

Lead Story

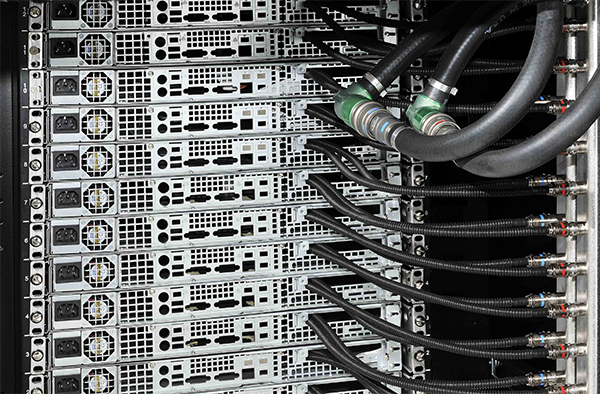

Heat is the bottleneck, and the AI buildout is industrializing HVAC

Chillers, CDUs, and heat exchangers are turning into strategic manufacturing capacity.

The AI boom is usually described as a chip race. That framing is now too narrow. The more consequential industrial question is how to remove heat continuously, at higher densities, with less tolerance for downtime, while still delivering projects on schedule. In practice, that shifts attention from GPUs to the physical systems around them: chillers, cooling towers, dry coolers, pumps, plate-and-frame heat exchangers, rear-door heat exchangers, coolant distribution units, liquid loops, valves, sensors, controls, and the factory-built skids that tie them together.

The scale-up case is already visible in the electricity data. Lawrence Berkeley National Laboratory estimates U.S. data centers used about 176 terawatt-hours of electricity in 2023, roughly 4.4% of national consumption, and could rise to 325 to 580 terawatt-hours by 2028 (6.7% to 12% of U.S. electricity use). The International Energy Agency puts global data-center demand at roughly 415 terawatt-hours in 2024 and projects about 945 terawatt-hours by 2030, with data centers accounting for nearly half of new U.S. electricity-demand growth through that decade.

Heat is the forcing function because higher compute density changes the economics of the mechanical stack. A conventional enterprise data center could often treat cooling as building equipment. AI facilities cannot. Once rack densities rise, the site operator is no longer just buying air handling; it is buying thermal assurance. That means more engineered systems, tighter controls, more factory preassembly, and more integration work between mechanical, electrical, and digital infrastructure. It also means more schedule risk if any one subsystem arrives late.

|

U.S. data centers, 2023

176 TWh

~4.4% of national electricity (LBNL)

|

|

IEA global, 2030 forecast

945 TWh

up from ~415 TWh in 2024

|

|

Modine data-center sales

+158%

year over year, latest quarter

|

The company evidence is catching up quickly. Modine reported a 158% year-over-year increase in data-center sales last quarter and disclosed a long-term agreement worth up to $4 billion to supply cooling equipment to an unnamed data-center operator, including a $165 million upfront payment to scale manufacturing capacity. Reuters reported this week that Schneider Electric expects its India data-center business to outgrow the rest of its local operations over the next four to five years; data centers already make up 15% to 20% of its India business, and much of the relevant equipment is locally manufactured.

Water is the second reason this matters. DOE's Federal Energy Management Program notes that cooling-tower systems are water-intensive and that water use scales directly with heat load and the efficiency of each stage of heat removal. Better hot-aisle and cold-aisle management can cut chiller energy by roughly 20%, which directly lowers cooling-tower water demand. The competitive set changes: the winners are not simply firms that can ship metal boxes, but the ones that can help customers reduce total site resource use while preserving uptime.

That is why the likely winners may not be the companies with the flashiest AI branding. They are the ones that can deliver integrated thermal hardware at industrial cadence. Cooling projects are increasingly constrained by fabricated sheet metal, brazed heat exchangers, pumps, controls integration, qualified field installation, and commissioning discipline. The constraint moves: coils, valves, racks, CDUs, epoxy, sensors, software, or trained technicians. Thermal equipment purchasing is starting to look a lot more like classic industrial capacity management, with localization following demand. Schneider's India footprint is one signal; expect similar logic across North America and Europe.

None of this eliminates risk. AI capex could cool. Efficiency gains could flatten part of the power curve. Water constraints and community opposition could defer some hyperscale campuses. But even those downside cases still support the same conclusion: thermal management has moved from background infrastructure to a front-line manufacturing category. The practical question for operators, suppliers, and investors is no longer whether the AI buildout needs cooling. It is whose factories can actually provide the thermal stack at the cadence this cycle demands.

Sources:

LBNL 2024 U.S. Data Center Energy Usage Report,

IEA via Reuters,

DOE FEMP,

Reuters on Schneider,

Investors.com on Modine.

|

|

How It Works

How direct-to-chip cooling actually works

Liquid cooling is not one product. It is a system of cold plates, manifolds, pumps, heat exchangers, valves, sensors, and controls.

|

- Capture heat at the chip. A cold plate mounts directly on the CPU or GPU package. Liquid running through it absorbs heat where power density is highest.

- Carry it to the CDU. The coolant distribution unit sits between the rack loop and the facility loop, using a heat exchanger, pumps, controls, and filtration to isolate rack-side chemistry.

- Hand off to the facility loop. Warm facility water flows to a chiller, a dry cooler, or in mild climates a water-side economizer that bypasses part of the refrigeration system.

- Reject heat outside. Cooling towers, dry coolers, or hybrid units dump the heat to the atmosphere. DOE notes water-side economizing can cut chiller use significantly during mild conditions.

- Measure and tune. PUE (energy) and WUE (water) track efficiency end to end. NREL's high-performance computing data center reports a PUE of 1.06 and a WUE of 0.7, per DOE-cited figures.

|

The manufacturing lesson

Liquid cooling is fabricated cold plates, hoses, manifolds, pumps, heat exchangers, valves, sensors, cabinetry, connectors, leak detection, and controls. More chips do not become more compute until all of that lines up. Throughput is an industrial assembly problem, not a single product.

|

Source:

DOE FEMP cooling-water guide.

|

|

Suggested Listening

TBPN, John Coogan and Jordi Hays

A daily tech livestream that doubles as a manufacturing news desk for the AI cycle.

TBPN, hosted by John Coogan (Soylent, Lucy, ex-Founders Fund) and Jordi Hays (Party Round / Capital), streams weekdays 11 a.m. to 2 p.m. Pacific on X and YouTube and posts to podcast platforms after. The New York Times has called it "Silicon Valley's newest obsession." For Manufacturing Monitor readers, the more practical pitch: TBPN spends a lot of airtime on the publicly-traded names that actually carry the AI cycle. Modine, Vertiv, Eaton, Trane, Schneider, Carrier, and the hyperscaler capex they ride get covered the day the tape moves, often before the trade press catches up.

When earnings prints from cooling and power suppliers start moving stocks 10% to 15% in a session, TBPN is usually the place where the framing solidifies in real time. It is not a manufacturing show. But it is one of the better daily reads on how Wall Street is pricing the physical layer of the AI build.

One tell about how strategic the AI-commentary layer has become: OpenAI acquired TBPN in April 2026, reportedly for low hundreds of millions, with editorial independence preserved. The AI cycle now owns the daily show that covers it.

Sources:

TBPN on Apple Podcasts,

CNBC on the OpenAI deal.

|

|

Last Pull

The AI buildout is industrializing HVAC. The next important manufacturing winners may look less like glamorous semiconductor names and more like the companies that know how to ship thermal systems on time, integrate them cleanly, and keep them running with minimal water, minimal drift, and minimal commissioning risk.

|

Reply with one line

Where is the next bottleneck hiding in your stack: equipment, controls, or commissioning labor?

|

Forward this to a colleague who lives on the floor. They can subscribe at manufacturingmonitor.com.

|

|